In search of Banksy, Reuters found the artist took on a new identity. “It appears that if people find a Banksy added to their wall, most of them call Sotheby’s rather than the police,”

So apparently we had a full-fledged Dreyfus Affair involving a billion dollar naval vessel getting torched and nobody acknowledges it.

As air power collides with geopolitical reality, the only certainty is that this conflict will permanently scar the Middle East. How did we get here and what happens next?

Welcome to The Uncomfortable, the brilliantly named brainchild of a Greek architect named Katerina Kamprani, who specializes in designing “deliberately inconvenient everyday objects.” My favorite is a fork with a chain handle (shown above), but almost all of her creations are clever, funny, and thought-provoking. Sometimes you have to see examples of bad design to make you appreciate how much we take for granted about gooddesign.

“Handbook on Guided Missiles” 1946 War Department report on German & Japanese rocket powered missiles & aircraft. This rarely-seen classic (scanned from a photocopy) provides a vast pile of information, including a great many diagrams. Air Doc 26 here. More.

Physician incomes are highest in the United States, and a decomposition shows that this mainly reflects differences in overall income distributions, rather than physicians’ locations in those distributions. This suggests that broader labor market differences, and thus physicians’ outside options, drive absolute incomes. Shifting US physicians’ incomes to match relative positions in other countries’ distributions would only marginally reduce healthcare spending.

Epic uses this to frame the entire suit as litigation-as-leverage rather than a genuine legal dispute. Perhaps that’s telling in some ways about respective company cultures- one saw it as an olive branch, the other saw a weapon. In any case, the optics intended could backfire, as judges generally do like seeing that a plaintiff tried to resolve things privately before burning judicial resources

The method is simple: set a goal, measure progress, verify against real records, repeat. The AI searches public archives, cross-references birth certificates against cemetery records against church books, and logs everything it finds (and everything it doesn’t).

The most incisive feedback from the docket argues that ONC’s historical focus on EHRs has created a structural failure in imaging interoperability. Because EHRs generally store only textual metadata or web links—not the multi-gigabyte DICOM files themselves—certifying the EHR accomplishes very little if the underlying PACS remains a proprietary, closed system Epic,

Awlaki, the New Mexico-born al-Qaeda cleric, was the first American citizen to be targeted and assassinated by a US government drone strike, in Yemen. Awlaki’s killing became a potent tool for radicalisation and inspired attacks by followers in the West.

I went to the New York Times to glimpse at four headlines and was greeted with 422 network requests and 49 megabytes of data. It took two minutes before the page settled. And then you wonder why every sane tech person has an adblocker installed on systems of all their loved ones.

A Mexican athlete said he was kidnapped and forced to compete for his life in a tournament of gangs. But was he actually playing a different game?

The math is simple and devastating. The United States has roughly 15 billion cubic feet per day of operational LNG capacity. Another 17 bcf/d is under construction. Another 19 bcf/d has been approved but hasn’t broken ground… the capacity Biden froze. If those frozen terminals had been approved on schedule in early 2024 and broken ground immediately, some would be approaching operational status in 2027-2028. Instead, they’re just now restarting the approval process after fourteen months of lost time.

The Globe and Mail sparked a debate when it reported that Canada’s GDP per capita has fallen behind Alabama’s. The comparison rattled Canadians and triggered a wave of criticism about the validity of using GDP per capita as a measure of national prosperity. Critics argue that GDP is a flawed metric, pointing to legitimate measurement challenges. But these measurement issues affect every country. The question is not whether GDP per capita is perfect but whether Canada’s trend relative to our peers signals deeper

In five or ten years, we may see almost no lending practices that resemble what is happening in this era. We will look back and say: that was a really bad way of conducting business. The question is whether we learn that lesson the clean way or the hard way.

William Faulkner once said, “To understand the world, you must first understand a place like Mississippi.” This week I had a chance to test that principle for myself, including a visit to Faulkner’s home in Oxford, Mississippi. I spoke at the University of Mississippi’s The Declaration of Independence Center for the Study of American Freedom about my book, “Rage and the Republic: The Unfinished Story of the American Revolution.” As I often do, I decided to take some pictures as I explored the campus and the nearby environs of Ole Miss. This is an extraordinary place filled with the nicest people you could even hope to meet. I could not recommend a visit more highly.

The circuit didn’t change. The contract between software and hardware did.

The AI ecosystem is fragmented. Developers often re-invent tool definitions, system prompts, and safety rules for every project. Skillware supplies a standard to package capabilities into self-contained units that work across Gemini, Claude, GPT, and Llama.

Traces of Evil aims to serve as a comprehensive digital archive designed to visualise the geography of the Third Reich for students, educators, and historians through innovative then and now photography and animated GIFs, mostly resulting from actually cycling to the locations. Established nearly two decades ago, the site juxtaposes modern photographs of obscure and prominent historic sites against their archival counterparts to render the past tangible and illustrate the physical evolution not just of locations associated with the Nazi Party and the Holocaust, but going back into time from ancient history and place.

Nations are increasingly weaponizing economic strengths. Edward Fishman’s 2025 bestseller, “Chokepoints: How the Global Economy Became a Weapon of War,” catalogues how governments increasingly leverage tools such as sanctions, control over critical technologies and financial restrictions to advance foreign policy goals. The U.S. exploits its dominant chokepoints (e.g. dollar-based global financial networks, advanced semiconductor technologies, maritime insurance & trade finance, access to western markets, sovereign assets held in dollars) to pressure Iran, Russia & China, among others. China has followed suit, leveraging its own asymmetric advantages (rare earth elements & critical mineral production, pharmaceuticals & medical supply chains, electronics manufacturing, EV batteries & green energy materials) to counter U.S. pressure and “punish countries who offend it.”

As Edward Coristine (aka Big Balls) told Jesse Watters last year, this was the “least peaceful” of all the agencies to deal with, and that it used taxpayer funds for private jets, an armory filled with weapons, and contracts with the former members of the Taliban (!!)

And the official Microsoft support page for “Outlook search not working” tells users to open the Windows Registry Editor and manually create DWORD values.

Apple also benefited from earlier foundational shifts. Building a $599 laptop under the constraints of Intel processors would have been extremely difficult. The transition to Apple’s own silicon — combined with macOS being overhauled to run on Arm-based processors — ultimately made the MacBook Neo possible.

Average cost in the U.S. to fully charge a Tesla Model Y Premium: $14.22 (up to 357 miles of range).

Average cost in the U.S. to fill up a Honda CR-V Hybrid: $48.30 (about 518 miles per tank).

The New York Times has now amended its “Smoking Jars of Metal and Fuses” headline, but it’s too late. Even in a world drowning in fake news, this particular masterpiece will live on in infamy.

The command structure is in freefall. After they killed a senior Hezbollah commander, the IRGC was so short on qualified personnel that they had to pull a retired general out of retirement, but the poor guy got killed almost immediately. You can’t make this stuff up.

Exxon, which has been incorporated in New Jersey since 1882, plans to ask its shareholders to vote on a proposal to redomicile in Texas. If successful, Exxon will follow Tesla, Coinbase Global and others that have reincorporated in Texas.”

Middle Eastern airlines and lessors have 1,710 airplanes on order. The Mideast represents 9% of Airbus’ backlog. It represents 14% of Boeing’s backlog. Airbus has a 43% share of the Mideast backlog, while Boeing has a 57% share. Embraer is a fractional player.

That, of course, was when he moved into the next phase of the attack. He texted me a link to review and cancel the “pending request.” The site, audit-apple.com, was a pixel-perfect Apple replica, and displayed the exact case ID from the real emails I’d just received. There was even a fake chat transcript of the scammers’ actual conversation with Apple, presented back to me as evidence of the attack against my account. At the bottom of the page was a Sign in with Apple button that he told me to use.

This is the lead “reporter” of that ridiculous CNN story. You will not be surprised to learn she uses “they/them” pronouns and graduated from Columbia’s journalism program.

The CBS News analysis reveals that over 700 of the roughly 1,800 hospices in LA County, trigger multiple red flags for fraud as defined by the state.

Junior and mid-level engineers can no longer push AI-assisted code without a senior signing off at AWS.

Yamaha Motor Corporation, known for creating motorized vehicles like motorcycles and WaveRunners, is set to relocate its headquarters to Kennesaw, Georgia, after more than 45 years in Cypress, California, where it first opened an office in 1979.

The hack occurred after a server at the Child Exploitation Forensic Lab in the FBI’s New York Field Office was inadvertently left vulnerable by Special Agent Aaron Spivack, who was trying to navigate the bureau’s complex procedures for handling digital evidence, according to the source and the documents.

Congratulations Apple on another insanely great product 50 years in the making.

People should be aware of these risks. I refused to run MDM software on any of my personal devices. The company needs to provide me with hardware if they want that. I personally isolate all corp devices to their own network too. If an adversary can get into the corp laptop, then can then get inside my network… there have been cases of it happening in the past.

The Chicago Transit Authority is deploying sheriff’s deputies on its trains, installing high-barrier entry gates to deter fare evasion, and starting “farecard inspection missions” after the agency’s federal funding was threatened.

The DfT has also allegedly attempted to conceal the document’s existence, despite requests made under Freedom of Information laws explicitly seeking its release. Ian Hudson is one of the few drone experts committed to uncovering further details about the Gatwick incident, and he has filed hundreds of these requests since 2018, including those that revealed the document’s existence.

After Schnur’s implosion with the revelation of his Stasi ties, the neophyte Merkel quickly accepted the patronage of Lothar de Maizière, member of a prominent family and the leader of the East German CDU. A respected figure, de Maizière headed East Germany for a few months in 1990 after the SED’s fall, in the run-up to national re-unification on Oct. 3 of that year. However, de Maizière’s cabinet post in Chancellor Kohl’s united government, a concession to German unity, collapsed a few weeks later when it was revealed from Stasi files that de Maizière, too, had informed for the MfS for decades as IM Czerny.

Former Secretary of State John Kerry, who once rhapsodized about geothermal and tidal power, has switched gears and endorsed nuclear.

I should be precise. They did not hack us. They logged in.

With patient, aligned capital and operators who understand both the problem and the business, we can build companies that the current financial market has decided not to fund. We can do it without losing money – in fact, we can generate real, compounding returns.

Reeling, Iqbal checked the news, where the shooting was being called an act of terrorism. The authorities had identified the suspect, Rahmanullah Lakanwal, as an Afghan refugee who had been part of the Zero Units — the shadow army of Afghan soldiers, funded and directed by America’s Central Intelligence Agency, that Iqbal himself had fought with for more than four years. Iqbal called his former intelligence chief, also now living in the United States, and asked him if Lakanwal had been part of their unit. The officer confirmed that he had, and so had his brother Ismail.

“The death of young Chadi Ammar grieves us deeply. He was part of our great family, who serve the most vulnerable with dedication and courage every day. His commitment and spirit of service will remain an example to us,” declared Grand Master Fra’ John Dunlap, expressing his sincere closeness to the family and all members of the Order of Malta in Lebanon.

Asked whether he feels compelled to follow the law on these matters, Fr. Rolland responded, “Yes, as long as the laws align with God’s laws, then it’s fine. It has been known in law from the very beginning that when the laws of the land and God’s laws conflict, God’s laws apply.”

Ryanair Refused To Pay A Delayed Passenger $1,182 — So A Bailiff Boarded Its Boeing 737 And Seized The Plane

In this piece, two researchers from PLA-affiliated National University of Defense Technology argue that Starlink will negatively impact global stability, in light of its clear military applications, increased risks of accidents and collisions in space, and SpaceX’s close relationship with the U.S. military. The authors foresee a worsening security dilemma as other countries react to broad U.S. deployment of Starlink, thereby impacting strategic stability in space.

“This story is fantastical and relies on false, unverified, anonymous claims.”

“Our Achilles heel, our blessing and our curse, is our bread,” co-owner Brian Perrone said.

Nothing about Operation Epic Fury occurred within a thousand miles of Tokyo. Yet no capital in the world stands to gain more from the wreckage of Khamenei’s regime than the one sitting across the East China Sea from Shanghai.

The results were stark. The range between the most expensive and least expensive mainstream supermarkets was a wallet-walloping 33%. If you counted warehouse clubs, the gap was even bigger. Those baskets carried the lowest price tags at Costco Wholesale and BJ’s Wholesale Club, both of which came in at 21% cheaper than Walmart.

As of February 23, 2026, of the 6,571 homes destroyed by the Palisades Fire in unincorporated Los Angeles County, a total of 13 homes have been rebuilt.

“I think it’s really, really nice to see a new shape. I do find (the barrels) appropriate,” commission member Jessica Klehr said. “I find them scaled well. And I think it would be thrilling to see this.”

Josh Mandel: Every patient has a right to their complete Electronic Health Information — but there’s rarely an API or in-portal button to request it. I built an AI skill that handles the request workflow via fax, finding the right form, filling, signing, and submitting with a cover letter explaining the request in vendor-specific terms. Here’s how it works, how to try it, and why I built it as a “Skill” rather than an app.

The City of Starbase is teaming up with SpaceX to help protect more than 1,000 acres of South Texas coastal plains through the Rockhands Mitigation Bank. A conservation committee will care for this land and ensure its wildlife and habitats are preserved for generations to come. SpaceX will provide funding and resources to support the City’s role as long-term caretaker, ensuring this unique coastal environment remains protected far into the future.

In the letter, Andy Walz, Chevron’s president of downstream, midstream, and chemicals wrote “the proposed regulation will cripple the survivability of the state’s remaining refineries.”

Both Sen. Susan Collins (R-ME) and Sen. Mark Warner (D-VA) ran for the Senate in 1996 by promising to never serve more than two terms, insisting career politicians are bad for the country. Here they are 30 years later, still haunting the Senate, seeking more and more years.

However, Murphy’s abandoned phone was picked up during the break and found to be recording. I was told the court yanked her press credential and sent her packing. Talk about contempt!

“It is definitely more expensive to shoot down a drone than to put a drone in the sky,” said Arthur Erickson, the chief executive and a co-founder of Hylio, a drone manufacturer in Texas. “It’s a money game. The cost ratio per shot, per interception, is at best 10 to one. But it could be more like 60 or 70 to one in terms of cost, in favor of Iran.”. Iran has fired off more than 2,000 one-way drones since the United States and Israel started attacking it on Saturday, and some reached their targets, despite billion-dollar air defense systems. It’s a looming problem — not just in the Middle East, but everywhere. In a world where attack drones are cheap, and defending against them expensive, the bill could become unsustainable over time.

The head of the Los Angeles Department of Water and Power stepped down Wednesday as part of a “planned leadership transition,” Mayor Karen Bass’ office announced. Janisse Quiñones, who took the helm at DWP in 2024, is returning to Puerto Rico, where she is from, to help modernize the island’s electric grid.

Preservation Chicago released its annual Most Endangered Buildings list Wednesday. The nonprofit, which advocates for the preservation of local architecture, has released editions of the list since 2003, spotlighting buildings and structures that are “endangered” by demolition or neglect.

Burchett asked Ellison why didn’t he prosecute these nonprofits criminally. Ellison replied in the moment that he has no power to do so. That answer from Ellison contradicted statements he made under oath earlier in the hearing, admitting he does have the power to prosecute frauds, including frauds other than Medicaid cases.

In 1979, Atari and Texas Instruments (TI) established a new category of computer, which hybridized the features of the personal computer and video game console. Like a video game system, they had dedicated graphics and sound chips and cartridge-based software, but they were also programmable and expandable, with peripherals like tape cassette drives and printers. But neither of their computers hit the “everyman” price point that would clearly put them in a new market segment—the Atari 400, at $550, cost nearly as much as two well-established personal computers (the TRS-80 and Commodore PET), and the TI-99/4 had a budget look but a premium price: at $1150, it was in the same ballpark as the Apple II.

“Over the next five years, he expects data centers to shift away from bespoke construction toward more modular, repeatable designs — standardized blueprints capable of being replicated globally at unprecedented speed.”

During the 2022 transformation of the former Glenway Golf Course into The Glen Golf Park, the focus was on making the course more accessible to first-time and older players while still offering a challenge to experienced golfers, Beck said.

I got to try two banh mi sandwiches at Dreamy Teazy this past week, a barely spicy sesame fried chicken and the more classic barbecued pork. This cafe at 1297 N. Sherman Ave. (next to a Klinke Cleaners) is making the best banh mi I have had in the city so far — crusty yet pillowy bread, lightly pickled radish and carrot, plus tangy mayo make this one of my absolute favorite sandwiches. They’re $12 and huge.

Considering your position, it would really be appreciated if you could engage in the Supreme Court race for Lazar. Post on Milwaukee restaurants really aren’t helpful in that regard.

A similar change has taken place in Venezuela. Once a star of world oil and one of the founding members of Opec, today it can hardly even be called a petrostate. It produces less oil than the US state of North Dakota and a quarter as much as neighbouring Brazil.

For decades, the abiding image of American healthcare interoperability has been the fax machine—a whirring, beige anachronism sitting in a basement medical records department, spitting out unreadable PDFs. But while policymakers were busy trying to kill the fax, a new and far more complex combatant entered the arena. The next era of health data won’t be defined by paper, or even by human beings clicking through portals and EHRs. It will be defined by “agents”—autonomous AI software designed to read, analyze, and act on medical records without a human ever touching a keyboard.

Meanwhile Massachusetts remains the only state in the country where the governor’s office, the legislature, and the judiciary have exempted themselves from public records law. They refuse audits. They refuse transparency. They refuse to enforce laws voters passed. This is how democrats “save democracy”

The NYT figured out that the way to fund journalism in 2026 is to make sure you can’t quit the crossword.

Consumer agents began to change how nearly all consumer transactions worked. Humans don’t really have the time to price-match across five competing platforms before buying a box of protein bars. Machines do.

WARN Firehose scrapes, normalizes, and unifies mass layoff notices from all 50 states into a single searchable database — updated daily. 109,000+ notices. 12.9M+ workers affected. Data going back to 1998. Available as interactive charts, bulk exports (CSV, JSON, Parquet), and a full REST API.

The Geometry of the Scoop; An overengineered interactive notebook exploring the differential geometry, materials science, fluid dynamics, and manufacturing topology of the Tostitos Scoops™ tortilla chip — arguably the most structurally sophisticated snack food ever mass-produced.

Within five years, Operation Breakthrough, the ambitious, but ultimately costly, delay-ridden and politically unpopular federal initiative that had propped up the Kalamazoo factory and eight others like it across the country, ran out of money. The dream of the factory-built house was dead — not for the first time, nor the last.

Over the past decade, I’ve worked to build the perfect family dashboard system for our home, called Timeframe. Combining calendar, weather, and smart home data, it’s become an important part of our daily lives.

The workflow I’m going to describe has one core principle: never let Claude write code until you’ve reviewed and approved a written plan. This separation of planning and execution is the single most important thing I do. It prevents wasted effort, keeps me in control of architecture decisions, and produces significantly better results with minimal token usage than jumping straight to code.

“The spending class IS the capital-owning class. The K-shaped recovery they fear actually stabilizes the demand base they say is collapsing. In the stable aggregate demand, the petit bourgeoisie finds ways to reinvent itself. I l ppl think the Citrini piece is excellent and worth reading. But history has repeatedly shown that periods of transformative productivity gains ultimately accrue to the consumer through lower prices, more leisure, and higher quality of life. Marx’s error wasn’t diagnosing the disruption, it was underestimating the system’s ability to adapt.”

The OpenClaw guy had five max subs and was losing 20k a month building and running his amazing project (because he was retired and had the money to set in fire) before AI labs banned this practice of having multiple subs. In case you just missed it: Because these agents are expensive as hell to run.

Keller and Abrams asked agents to eschew the doom and gloom of the current moment — home sales, they said, will likely be no better than 2025 — and think about the market in historical cycles, which show home values tend to trend up, building a solid source of wealth for homeowners. “Feelings — do not look at that,” Keller said. “Work with facts.”

Why should you care if you don’t own a tractor? Because when a combine goes down in the middle of harvest, it means fewer acres cut before the rain hits. It means grain that doesn’t get hauled on time. We like to imagine the food supply as a smooth conveyor belt. In reality it’s tight timing, thin margins, and a lot of heavy machinery that increasingly runs on proprietary software.

Understanding why businesses actually fail matters regardless of where you sit politically, because it is a matter of short- and long-term governance. When a retailer fails, state and local governments pick up the tab: lost sales tax revenue;, unemployment insurance claims, economic development incentives to attract replacement employers. If those failures are driven by demand shifts, that spending is a reasonable cost of economic transition. If they’re driven by capital structure decisions made at acquisition, taxpayers are subsidizing the back end of a private transaction they had no part in. If we misdiagnose Joann as a story about consumer preferences or e-commerce disruption, every downstream decision, from unemployment policy to pension allocation, starts from the wrong premise.

The initial architecture focused on brutal simplicity. I persisted a flat list of components that I would manually place by first sketching it out in Photoshop, and every frame the engine ran a minimal loop:

From a strategic standpoint, the US is not just an additional destination but a high-value test case for India’s transformation from a regional production base into a platform for global market access.

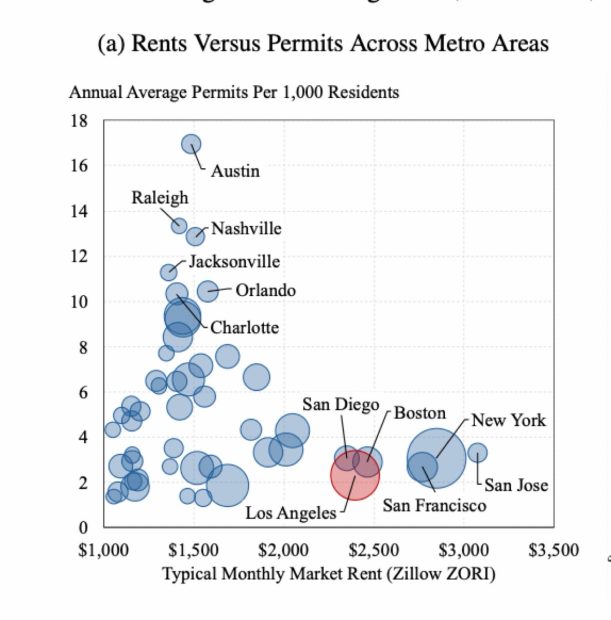

Permitting costs are widely cited, but little analyzed, as a key burden on housing development in leading U.S. cities. We measure them using an implicit market for “ready-to-issue” permits in Los Angeles, where landowners can prepay permitting costs and sell preapproved land to developers at a premium. Using a repeat-listing difference-in-differences estimator, we find developers pay 50 percent more ($48 per square foot) for preapproved land. Comparing similar proposed developments, preapproval raises the probability of completing construction within four years of site acquisition by 10 percentage points (30 percent). Permitting can explain one third of the gap in Los Angeles between home prices and construction costs. Keywords: building permit, land-use regulation, hedonic, zoning, capitalization. more.

We’re slowly losing one of the things that makes tennis genuinely great, surface diversity. This doesn’t show up in most audience analysis. In part because the creep of hard courts has been gradual, but also because it’s impossible to miss what you haven’t experienced. But there is an opportunity cost to having great players mostly ply their trade on one rather than three more evenly split surfaces, and an even greater cost to junior players optimising mostly for a hard court tour rather than a grass, clay, and hard court environment.

…The future of Substack is going to tilt toward writers with large audiences running completely unregulated pump-and-dump schemes through prediction markets. Buy low, tell your readers why X outcome is undervalued, sell high, pocket the difference. Not all Substack writers will make use of the Polymarket widget. But if you want the company to algorithmically promote your content, maybe you should try out this hot new gambling trend.

The cyberattack on Change Healthcare, first detected in February 2024, has grown into what appears to be the single largest exposure of personal health data in American history. UnitedHealth Group, the parent company of Change Healthcare, has estimated that approximately 190 million people were affected by the breach, a figure that dwarfs every prior federal data incident on record. The scale of the compromise, the simplicity of the initial intrusion, and the cascading disruption to medical billing and pharmacy systems across the country have forced a reckoning over how the nation’s largest health conglomerate secures the data of more than half the U.S. population.

The first is Audio Transcription in Notes. It records audio, transcribes it in real time, and summarizes the whole thing into key points. It’s built for meetings, lectures, interviews, and anything you want to capture and keep. The second is Live Captions. It transcribes any audio playing on your phone, or any sound happening around you, in real time. FaceTime calls, YouTube videos, podcasts, someone talking to you across a table. It works across every app on your phone and it doesn’t record anything. It just puts live subtitles on your screen.

LASIK eye surgery cost $2,200 per eye in 2000. Today it’s around $1,000 per eye despite 24 years of inflation. Meanwhile, an MRI that cost $1,200 in 2000 now costs $3,000+. The difference? LASIK operates in a free market with no insurance interference and minimal regulation.

New research shows that seasoned birders — including older adults — had denser tissue in parts of the brain tied to attention and perception.

But when his homegrown remote control app started talking to DJI’s servers, it wasn’t just one vacuum cleaner that replied. Roughly 7,000 of them, all around the world, began treating Azdoufal like their boss.

This article contends that the PE investment model imposes social costs in many portfolio companies through over-leverage, value extraction and short-term incentives. Part I shows how debt-driven acquisitions increase the probability of restructurings and job losses. Part II analyzes how profit pressure in PE portfolio companies can harm third parties including workers, healthcare patients, consumers, unsecured creditors, communities and the environment. Part III proposes limited, specific reforms—insurance and bonding requirements, minimum staffing and quality regulations, and increased disclosure requirements focused on sensitive industries and service sectors—that would require PE funds to internalize these foreseeable harms and provide federal and state regulators with the tools to identify and minimize related risks. This article concludes that these modest but targeted changes can preserve the benefits of the PE investment model while materially reducing externalized costs.

The Trump administration received at least 21 ideas to revitalize @Dulles_Airport. All would keep Saarinen’s iconic terminal but most would turn it into a ceremonial space with a new departures terminal elsewhere on airport grounds.

“South America has never offered me a deal good enough to seriously consider it. The Middle East has always been much better in terms of appearance fees. The European swing has also provided strong financial incentives. That makes a difference,” Tsitsipas, the former world No. 3, told CLAY.

Jane Street is also where SBF learned to trade before founding FTX and Alameda Research, and many of his future colleagues came from the firm or intersected with its networks. According to the lawsuit filed by Terraform’s bankruptcy administrator Todd Snyder, Pratt became the bridge between his former employer and his new one through a chat group that court filings describe as “Bryce’s Secret.”

The Gigacasting race isn’t just about tonnage. It’s about achieving the highest part reduction with the largest casting manufactured with the leanest process.

Pre-pandemic: ?,??? ????????? ??? ??? ??????? ??????. FY2025: ?,??? ????????? ??? ?? ??????? ??????. That’s 15% more staff serving half the customers. Per-employee comp is up 32%, from $140K to $171K. Any private company that lost half its customers and then grew headcount would be bankrupt. BART just asks for a tax increase.

Legacy platforms look very different. A typical mid-to-high-end vehicle still carries 70–120+ ECUs. The intelligent functions are spread across many specialized modules from multiple Tier-1 suppliers. Here is what changes when you drop in the Tesla box: Net effect: One Tesla box replaces the functional equivalent of 8–15 major ECUs or Tier-1 subsystems.

For the second year in a row, Trader Joe’s was the cheapest place to shop for groceries — this time by an even more significant margin. The same bag of items cost less than half as much as at Bi-Rite, this year’s priciest store. Independent grocers such as Mollie Stone’s, Luke’s Local and Gus’s Community Market all saw increases, though to varying degrees. We found nearly the exact same prices for most items at Safeway and Trader Joe’s as last year. Lucky was the only supermarket that saw decreases, though they were slight. (The Chronicle didn’t visit value-driven stores Grocery Outlet and Costco because of their inconsistent offerings, and omitted international grocery stores for the sake of direct comparison.)

The relevant bottleneck for humanoids is not “rare earths” in general, but the NdPr-to-magnet supply chain. China’s dominance in midstream processing and magnet manufacturing gives it leverage over the pace, cost curve, and industrial geography of embodied AI.

Massachusetts, long a bastion of progressive politics and high taxes, has quietly watched the equivalent of one-and-a-half Cambridges pack up and leave. A new analysis from the Pioneer Institute finds that more than 182,000 net domestic residents exited the commonwealth between April 2020 and July 2025, a sustained outflow that researchers describe as a lasting structural shift rather than a brief pandemic aftershock.

“If I recall, the timing between Apollo 7 and 8 was nine weeks,” the official said. “Launching SLS every three and a half years or so is not a recipe for success. Certainly, making each one of them a work of art with some major configuration change is also not helpful in the process, and we’re clearly seeing the results of it, right?”

If Big Tech organized as a class, they could do it effortlessly, at personal costs they would hardly notice — but it’s obvious to anyone with even passing familiarity with these people that they will never do anything like this. Elon Musk is by far the most radical and iconoclastic of the Silicon Valley billionaires, and he’s nowhere near this — which would, itself, be an embarrassingly petty exercise of political power by the standards of the wealthiest men in history. (Or even in comparison with the industrialists of the turn of the 20th century.)

Covey died in a cycling accident in 2013, at fifty. When Bezos wrote about her afterward, the word he chose was not talented or dedicated. He said she had “a deep keel.”

The @SFBART board should be held responsible for their unconscionable mismanagement of the transit system, spending like drunken sailors as ridership plummeted by half, adding $100 million in new staff alone for an emptying system. Now they’re playing the nihilism doomsday card.

And with it came a pernicious culture that religiously believed that words, be they diplomas or diplomatic cables, defined reality. Not actions. Or physics.

Best advice you can now give Danish entrepreneurs is to leave the country before anything gets off the ground. Danes better hope Novo never falters.

Still, the liberal interventionist—and Catholic—in me approves: commit the sin, ask for forgiveness later. More crudely stated: always kick ’em when they’re down, because God knows they’d do the same to you.

This is a drone cargo plane, designed for logistics and disaster response. It is the first unmanned aircraft for high-altitude, it can operate using very short runways, and is adaptable to either landing full of cargo, or dropping it by parachute to the ground. The capacity is one ton, with a range of over a thousand miles, with AI systems for loading and unloading in under five minutes.

The international order follows the law of the jungle much more than it follows international law. There are five major kinds of fights between countries: trade/economic wars, technology wars, capital wars, geopolitical wars, and military wars. Let’s begin by briefly defining them

Rummler/Obama covered up the prostitution scandal, and instead blamed the Secret Service: ten members lost their jobs over the scandal.

These developments do not represent isolated events but markers of an industry shifting toward broader participation, tighter regulatory scrutiny, and more strategic use of airspace management. The trajectory of drones in the next 12 to 24 months will be shaped as much by policy choices and manufacturing strategy as by technical innovation.

4 Charity suffereth long, and is kind; charity envieth not; charity vaunteth not itself, is not puffed up,

It also revealed the lack of talent on the Democratic team. You may have seen the clip of AOC trying to answer a question about U.S. support for Taiwan–a question that foreseeably is likely to come up, but about which she evidently has never spent a single moment thinking:

From below, hundreds of AI-native startups are entering every vertical. When building a credible financial data product required 200 engineers and $50M in data licensing, markets naturally consolidated to 3-4 players. When it requires 10 engineers and frontier model APIs, the market fragments violently. Competition goes from 3 to 300

Great quote from the owner… “There are towns across America that wish they were Music City — and we’re trying to be Las Vegas. Why?”. Absolutely terrible quote from the mayor. “ It’s not up to me whether he keeps that business open, the market evolves.”

(Yes, a human still decides which tools the agent is allowed to use. That’s a real marketing surface. But once the agent is running, the runtime purchasing decisions are pure optimization. The land grab is making it onto the allowlist, then being the best option once you’re there.)

This buy-then-convert pattern turned out to be surprisingly common. Using searches of Becker’s, CHOW, and hospital finance websites, I found 25 cases of for-profit hospitals getting acquired by nonprofits in the last decade. In over half those cases, the newly acquired hospital almost immediately (within a year) enrolled in the 340B Program. The remainder did not enroll because they were not 340B-eligible even after conversion (e.g., they did not meet eligibility criteria such as the DSH threshold). Here’s the full timeline of the acquisitions I found:

These findings suggest economic policies implemented in the 1970s had nothing to do with the Midwestern population declines that occurred after the 1970s. Rather, these data are consistent with a long-term and large-scale shift in preferences that began long before the 1970s, one that was not unique to the Midwest. It is foolhardy to center public policy around this false narrative, and, unsurprisingly, the administration’s attempts to reverse this trend have not only failed but have also economicallyhurtAmericans.

Companies report that they face a “reviewer lottery,” where critical questions hinge on the approach of a small number of individuals at FDA. Some FDA review teams are creative and forward-leaning, helping developers design programs and overcome obstacles to get needed products to patients, without cutting corners. FDA’s Oncology Center of Excellence (OCE), for example, is repeatedly identified as a model for providing predictable yet flexible options for bringing new drugs to cancer patients. OCE is now a dialogue-based regulatory paradigm that has facilitated efforts by academia, industry, the National Institutes of Health (NIH), and others to develop new cancer therapies and launch innovative programs and pilots like Project Orbis, RealTime Oncology Review.

He then goes on to list what he thinks is going to happen, for which the point summaries are:

• There will be more software than ever before • AI-enabled or AI-centric software is simply moving up the stack of what a product is • New tools will be created with AI that do new things • Domain experience will be wildly more important than it is today because every domain will become vastly more sophisticated than it is now • Finally, it is absolutely true that some companies will not make it.

The Circle Pines man worked for the Minnesota Department of Corrections until this past October. As wild as Brown’s story is, this is even wilder. Department of Corrections Commissioner Paul Schnell thanks the immigration authorities for their efforts. “If these federal allegations are accurate, this individual engaged in sophisticated efforts to misrepresent their identity, extending well beyond Minnesota,” Schnell said. “We are grateful to USCIS and ICE for their work in investigating and addressing immigration fraud.” Now that is wild.

But here’s what should keep software founders up at night: the line only moves in one direction. Every model generation pushes it higher. What’s above the line today will be below it in eighteen months. You can’t build a business on the assumption that your moat is permanent when the water level is rising on a schedule.

Business has never been better for lobbyists paid to push the agendas of foreign countries and companies, but critics say the surge undermines Trump’s ‘America First’ pledge.

“One third of the total package price, with the land, is in the regulatory costs,” one builder noted, including “your wetland fees, your park dedication fees, your permit costs,” and more. Thus, a house in Corcoran, Minnesota, that costs $182,000 to build will have an all-in cost of $372,000, including $56,000 in administrative costs alone! Throw in a modest profit margin, and you’re well out of “starter” range in the area. The same goes for estimates from Michigan and New Jersey.

The New York Post published their reporting three weeks before the end 2020 presidential election. Within 48 hours, 51 former intelligence officials signed a letter calling it likely Russian disinformation. They knew it was authenticated. They coordinated with the Biden’s Autopen campaign to sign it anyway. Twitter locked the New York Post’s account. Facebook suppressed the story. The corporate media called it a smear.

Chinese carmakers have lower cost structures, driven by tighter control over their supply chains and a stronger focus on the China market. This puts Western OEMs in a tough spot.

Putting data into glass is as simple as etching it (to be clear, this is technically not etching, which is a chemical modification of glass’ surface—here, lasers burn features into the interior of the glass). But that’s been one of the challenges, as the writing is typically a slow process. However, the development of femtosecond lasers—lasers that emit pulses that only last 10-15 seconds and can emit millions of them per second—can significantly cut down write times and allow etching to be focused on a very small area, increasing potential data density.

But there was something special about the original M5, launched in spring 1985, and it wasn’t only that it was the second car after the M1 to use the two-digit model code and get a proper WBS motorsport prefix on the VIN plate. Almost four decades later, there’s still something magical about the M5, and it remains the car that’s referenced as ground zero when it comes to super saloons.

David Reichel, executive director of the Sierra Avalanche Center, explained that the conditions became lethal as the massive storm delivered heavy snow on top of a base that had been transformed by an exceptionally dry January and start to February. The fresh snow, he said, fell on a “layer of snow that weakened and became unstable during the warm, dry weather.”

Drawing on OBFCM data from ~1 million vehicles (2021–2023), it reveals significant gaps: PHEVs emit 3–5 times more CO? than approved, with only ~25–30% electric driving due to frequent combustion-engine use even in battery-discharge modes. 2. Average real fuel consumption for PHEVs is 5.9 l/100 km, comparable to pure combustion-engine vehicles, undermining their climate benefits.

More Billing Codes See Skyrocketing Billing. T1019 is not the only billing code with explosive growth from 2018 to 2024, although it is the code with the highest amount paid out in that time. Twenty-two other codes saw anywhere from 200% to over 10,000% increases. Eight codes had over 500% more payments.

The old view: Everything is gray, no absolute right or wrong.

The new reality: Scripture provides clear guidance — God doesn’t leave us hanging.

Why it matters more now: As technology and human power to manipulate nature grow, objective morality (rooted in Scripture) becomes essential to stay grounded and good.

Result: Life feels better, clearer, more filled with light when aligned with unchanging truth.

I know that’s uncomfortable. Code review is sacred. It’s how you catch bugs, share knowledge, maintain standards. It’s also an identity thing. We’re engineers, and reviewing code is what engineers do. But clinging to the PR workflow in an agent-driven world isn’t rigor. It’s an identity crisis. Think about it. An agent generates 500 PRs a day. Your team can review maybe 10. The review queue backs up. This isn’t a bottleneck worth optimising. It’s a fake bottleneck, one that only exists because we’re forcing a human ritual onto a machine workflow.

The next morning, I rode back to the same crumbling building where I’d been polygraphed the day before. The examiner said, “Now that you’ve had a chance to think about it, is there anything you’d like to say?” He didn’t need to ask me twice. “You bet there is. I did my part, now I expect you to do yours.” It wasn’t until late that afternoon, when I was waiting for my plane at Dulles, that I realized, “Is there anything you’d like to say?” does not mean, “Please tell us all our faults.”

The concept behind sandboxing is fundamental to modern security: by restricting what an application can access, you minimize the potential damage from malicious code or unintended behavior. Think of it as putting an application in a secure room where it can only interact with specific objects you’ve placed there.

It’s already showing up in the numbers. Earlier this month, the FT reported that KPMG pressured its own auditor, Grant Thornton, to cut fees — arguing that AI should make the work cheaper. Grant Thornton agreed to a 14% reduction. When a Big Four firm is using AI as leverage to renegotiate its own audit fees, the repricing isn’t theoretical.

Looking around, and given that the high level idea is clear, there are a lot of smaller Claws starting to pop out. For example, on a quick skim NanoClaw looks really interesting in that the core engine is ~4000 lines of code (fits into both my head and that of AI agents, so it feels manageable, auditable, flexible, etc.) and runs everything in containers by default. […]

The career path of most application programmers is fairly short. In most enterprises, the majority have five years or less of real in-depth experience, and battle-scared twenty-year+ vets are rare. Mostly, these novices are struggling through early career experiences, not ready yet to deal with the unbounded, massive complexity present in a big design.

And, then there’s the blatant fraud… for which I sadly don’t expect any final accounting and punishment.

“The term [provider] should not be used to describe physicians, nor should physicians use it to describe themselves, their team members, or their trainees.”

The H-1B program lets firms hire high-skill foreign workers for a six-year term. The annual number of visas allocated to for-profit firms is capped at 85,000 and there is excess demand for those visas. The analysis merges data from the Labor Condition Application where firms attest that H-1B hires do not adversely impact natives, the I-129 Petition for a Nonimmigrant Worker where firms request to hire a specific person, and the American Community Surveys. On average, H-1B workers earn 16 percent less than comparable natives. The payroll savings suggest that firms may be willing to pay a one-time fee to obtain an H-1B visa. The data are examined using a labor demand model to simulate how a fee alters the hiring decision. Depending on the level of excess demand, the unobserved productivity gains or costs from an H-1B hire, and the rate of job separations, the revenue-maximizing fee is between $118,000 and $264,000, has little or no impact on the number of H-1Bs hired, and generates between $6.2 and $22.4 billion in revenues. The fee would also change the skill composition of the H-1B workforce, making it more skilled.

In November 2025, the EU’s trade deficit with China averaged €1.07 billion a day. EU imports from China rose 4% year on year in November 2025, while exports fell 1%. As a result, the EU’s trade deficit with China widened to €32.2 billion, up from €30.3 billion a year earlier.

Matyushev says the Kona needs $250m for development, certification, and EIS. LNA estimates that upwards $900m is a closer figure. Matyushev says the Horizon needs $3bn to $5bn, a figure LNA estimates is significantly under-estimated. JetZero says it needs $7bn to $10bn for the Z4. LNA also believes this number is way too low.

Geely may be best placed to build cars here: Volvo Cars, which it controls, has had an auto plant up and running in South Carolina since 2018, where it builds Volvo and Polestar vehicles. (Volvo stated, “We do not have any plans to produce cars on behalf of Geely there.”) If Geely does attempt to enter the US market under its own brands, it likely won’t happen before 2029.

Yiannis Exarchos, the CEO of the Olympic Broadcasting Services (OBS), told reporters Wednesday that 15 FPV drones are being used in Milan Cortina, with an additional 10 traditional drones aiding coverage (it takes 800 cameras in total to broadcast the Games, per the OBS media guide). The use of FPV drones, Exarchos said, helps make sense of some of the more unconventional winter sports — particularly to casual viewers who only tune in during the Olympics.

But now, the market is shifting again. We are at an inflection point. The geopolitical architecture that allowed Taiwan to become the sole foundry for global democracy is looking brittle. The “Silicon Shield” is looking less like a shield and more like a target. The world needs a backup drive. And surprisingly, the coordinates for that backup drive are pointing to a snowy plain in Northern Japan.

Starlink has grown its customer based from around 10,000 in 2021 to around 4,000,000 by October of 2024.

It’s all state-of-the-art. And it’s terrible. Light switches, which have been self-explanatory since the dawn of electric lighting, apparently now come as an unlabeled multibutton panel that literally required a tutorial session from a technician. Pressing the same button twice might turn the lights on and off, or you might have to press one button for “on” and another for “off.” “It depends” is the name of the game—which is exactly what you don’t want when you’re trying to find the bathroom in the middle of the night.

“This is due in large part to the high construction costs of smaller-scale buildings for each home created,” the report says. “However, recent changes allowing construction of small multiunit buildings in most of Madison’s residential areas may contribute to an increase in this construction type in coming years.”

Alphabet (google) has lined up banks to sell a rare 100-year bond, stepping up a borrowing spree by Big Tech companies racing to fund their vast investments in AI this year.

$1T in Medicaid provider spending data released on opendata.hhs.gov. Public should know how its money is spent! Data explorer.

A fireplace is consistently among the most-searched amenities by home buyers nationwide, according to Zillow. But while convenience leans toward the automated ease of gas, many wealthy homeowners prefer the sensory trifecta of real fire: the scent, the rhythmic crackling and the living warmth that a faux flame simply can’t mimic. “The more high-end the property is, the more the homeowner typically wants it,” says Katherine Koriakin of Wyoming’s GYDE Architects.

The trend of construction productivity in the United States failing to improve over time is indeed concerning. “Productivity” means some measure of output, divided by some measure of input. When productivity is improving, we get more output for a given amount of input over time; if productivity is falling, we get less output for a given amount of input over time. If productivity doesn’t improve, we can’t expect construction costs to fall and things like houses, roads, and bridges to get any cheaper. Because of this, it’s worth looking deeply at what exactly the trends in US construction productivity are.

But it’s all an illusion. Artificial enchantment. Virtualized nostalgia. It may sound like you’re ripping revs from gear to gear—HHHHM, HHHuuum, Hummmmm. But the revs you hear, and therefore the reality you can faithfully report, is completely artificial. The damn thing doesn’t even have a transmission, per se.

Yes, this is all boring. No sane person should ever get excited about a blank wall, let alone read a thousand plus words on the subject. But your wall at home is a recurring reminder that most true architectural and design advancements are almost entirely invisible.

Yeah, I’ve been relatively quiet not for lack of effort, but because I’ve been hard at work automating myself using OpenClaw. Not for the boring (and socially risky) use cases of social media or email monitoring. No, I set to build a full-fledged research assistant that has access to FEC records, 990s, and has a strict entity resolution pipeline. Every question I ask it, it gets smarter because it automatically rolls in its own discoveries to the various graph databases it has.

Poland did this in 1989 under Balcerowicz. Two years of pain, then 28 consecutive years of growth. Argentina has attempted this playbook before and failed. Milei’s bet is that he can hold the political coalition together long enough for growth to materialize.

“The competitive reality is that the Chinese are the 700-pound gorilla in the EV industry,” Ford CEO Jim Farley told me in an interview last year. “There’s no real competition from Tesla, GM or Ford with what we’ve seen from China.” Even Farley, after driving a Xiaomi SU7, said he didn’t want to part with it. The company is now rebuilding its EVs, starting with a $30,000 pickup, to compete directly with what they have seen from China.

And yet, this is how a lot of modern software behaves. Not because it’s broken, but because we’ve normalized an interruption model that would be unacceptable almost anywhere else.

The Dot-com Optimists Got a Lot Right. An analysis of Mary Meeker’s late-90s internet reports suggests she was often accurate, or even too conservative.

With launches every hour carrying 200 tons per flight, Starship will deliver millions of tons to orbit and beyond per year, enabling an exciting future where humanity is out exploring amongst the stars.

As with the large number of ‘blatniks‘ in the Soviet era who made sure their factories got what they needed outside the formal state procurement process, Epstein greased the wheels for the neoliberal state. His job was governance.

Publishing industry progressives were shocked that Frederick would even consider calling the police on black people (angelic children, probably) so soon after the killing of George Floyd. She was basically murdering them. Under intense pressure, everyone who worked at the agency resigned.

The Minnesota welfare fraud story isn’t an immigration story or a story about an excessively generous welfare state. Rather, these thefts were the predictable result of a public policy decision to embed middlemen throughout our welfare system. Like many frauds that pop up all across the country and the welfare state, the Minnesota day care schemes all occurred in programs where a private provider acts as a middleman between the government and individuals.

It’s all part of the airlines’ ongoing fight for market share and access at O’Hare, where the Chicago-based United has the hometown advantage and more gates. It intends to squeeze out its rival, but American, headquartered in Fort Worth, Texas, is just as determined to maintain the airport’s status as a dual hub. After all, O’Hare’s central U.S. location makes it a premier spot for domestic and international connections. “It is one of the few airports in the world that genuinely is able to be home to major airline alliances,” says John Grant, chief analyst at the travel data company OAG.

Industry analyst Robert Mann Jr. characterizes the conflict as a battle of press releases and big egos: “Mr. Kirby is attempting to essentially extend United’s lead in Chicago, and this put up a marker for [American CEO] Mr. [Robert] Isom, who has decided that he would like to even the score.”

Now a fair and necessary taxpayer question: Can Hennepin County confirm that local property tax dollars are not funding excessive executive compensation packages at contracted nonprofits? For reference, Nexus Family Healing’s IRS Form 990s are public records and should be part of this discussion:

The report concluded that “no one knows whether there are other unknown biolabs because there is no monitoring system in place.” Now we know that there was at least one other, but we still don’t know how many more. That is why it is critical for Congress to pass my bipartisan legislation, authored with Rep. Costa and Rep. Valadao, to find these labs and shut them all down.

While Thiel is fond of Britain, he believes we have made serious errors by not controlling our ‘crazy immigration’ or taking advantage of the tech-powered growth the United States has. Nonetheless, he hopes that Britain can stand up to a vengeful American administration if the Democrats are elected in 2028, perhaps even acting as a refuge for the politically persecuted. In this sense Britain is like New Zealand, where Thiel has acquired citizenship and bought land to help him establish a refuge in times of international discord.

Submitted: “Our trash removal drivers got 2 seat belt violations in downtown Minneapolis this week, in case you wanted to know what Frey’s police force is actually working on.”

“At this point, they bring nothing but baggage,” one Democratic lobbyist told the publication. The Clintons’ “continued presence is a barrier to the party’s renewal,” the lobbyist said.

“I was hired by the Washington Post in 2021 transcribe all our interview questions and give them to Joe Biden days in advance on picture post cards.”. “Today I was laid off.”

If your position at The Washington Post was recently eliminated, please consider applying to write for The Babylon Bee. We are seeking applicants experienced in writing fictional content presented in the tone and style of a legitimate news organization.

As usual, the answer is: upskill yourself and adapt. If a crusty old fart like me can do it, you can too.

The problem is that it has given me no reason to care about possessing a short understanding of where early Venice came from. “There are lots of cities out there—so what?” No matter what material the author might cover after this historical background introduction, only the most dedicated readers will make it that far.

This map shows active Coast Guard navigational beacons in the United States and parts of Canada, from the 2025 Light List.

The Signal network erupted. Using a red phone emoji to signal an all-points alert, a message blasted out: “?? easy. URGENT: observers urgently requested at glam doll donuts @ 26th & nicollet [sic]. an observer has been shot by ice, unknown condition, emts [emergency medical technicians] present, please be safe. EDIT: medics requested to join perimeter in case agents start gassing. be aware there are many agents and mpd [Minneapolis Police Department] officers present.”

One unlikely beneficiary has been the British Overseas Territory of Anguilla, which lucked into a future fortune when ICANN, the Internet Corporation for Assigned Names and Numbers, gave the island the “.ai” top-level domain in the mid-1990s. Indeed, since ChatGPT’s launch at the end of 2022, the gold rush for websites to associate themselves with the burgeoning AI technology has seen a flood of revenue for the island of just ~15,000 people.

Vimeo stock IPO’d at $52, and within a year, lost 85% of its value, trending down to just $8.42 by the end of May 2022. As we entered 2022, many states and localities had started easing up on lockdown restrictions, which hurt not just Vimeo, but many other tech companies as well. By the end of the summer of 2022, the tech sector had entered an unspoken recession, encasing the carnage at Vimeo in a cement tomb that it’d never be able to break free from.

You can trace all the funding mechanisms you want, but at the end of the day, the trail will end at the CIA/NED/USAID’s doorstep.

What I’m trying to say is, the same way Americans need to visit the world and find meaning, we need them to come, to flood us like some contrast liquid and give us meaning.

The jumpers will arrive Feb. 1 and stay with the family through Feb. 10. The Slovenians will return to Westby after jumping in the Norge tournament near Chicago. “They have several other tournaments in the U.S. after the Snowflake tournament, but they wanted to come right back to Westby in between and we are excited to have an extra few days with them.”

The boy who cried wolf is a cautionary tale about false alarms. But there’s another version of that story: the village that was so conditioned to ignore warnings that they didn’t notice when the wolf actually showed up. Look at the evidence. Draw your own conclusions. And if those conclusions match mine, then we have work to do—and the time to start is now.

For the adventurous, the answer is: today. Both MapLibre GL JS and MapLibre Native now support MLT sources. You can use the new encoding property on sources in your style JSON with a value of mlt for MLT vector tile sources.

Third, Christians must not be intimidated by the vitriol of our opponents. These are dark and serious times for the church in America, but we must remember that we are blessed when others revile us and when they lie about us (Matthew 5:11-12). In this life, we will have enemies because Christ Himself has enemies. Such opposition is not a sign of failure, but an invitation to greater faithfulness. The enemy’s tactics are not new, and they cannot stop the advance of Christ’s church. The darkness cannot overcome the light.

But there was one last hope to save the team. In December, a group of Buffalo businessmen, key leaders in the community, came to Sonju with a proposal: If we sell 2,000 more season tickets for the remainder of the season, will John Y. Brown promise to keep the Braves in Buffalo? Sonju asked Brown; Brown said yes. A massive 30-day blitz began, with the Buffalo bigwigs knocking on doors and holding out their hats. All they needed was 2,000 season tickets to save the Braves. They sold less than 100.

Then comes the Palisades fire and guess what? The insurance companies are now suing the Government of California because they think California should pay…not them.

The NTSB has released an animation reconstructing the final three minutes before the midair collision near Washington D.C., illustrating what each crew could—and couldn’t—see at night and why see-and-avoid measures failed.

On Jan. 5, Walz shocked the political world by suddenly — and angrily — dropping his re-election bid, connecting his decision directly to the attacks he’d sustained, starting with the recent wave of fraud coverage. According to Axios, it was actually “fellow Democrats” who applied the “mounting pressure” that forced the governor’s hand.

Football is a purely mediated experience, even when there is no media involved. It’s not just that you can see a game better when you watch it on television. Television is the only way you can see it at all.

“DO NOT make the mistake President Biden made for not firing a grossly incompetent DHS Secretary.”

City of Oakland managed by clowns. Imagine in 2013: new venues for the A’s, Raiders and Warriors. 2026: Everyone left, and nobody even wants to buy the emptied out husk of land. Local elections matter. Pay attention to local elections and hold your local leaders to account.

They are also a good example of what their proponents have labelled “gentle density”, offering five or six storeys of space-efficient housing, laden with attractive and practical period features.

He was once married to a Patrice Kazmierczak. They divorced a few years ago. His ex-wife Patrice is a political activist & a big supporter of Ilhan Omar & AOC.

Rams is a documentary portrait of Dieter Rams, one of the most influential designers alive, and a rumination on consumerism, sustainability, and the future of design.

Oliver would get up before dawn and use small fish colloquially known as poagies to lure lobsters from her boat, the Virginia, which was first owned by her late husband. As she established a remarkable 97-year tenure on the waters, and word of it spread, she became the subject of documentaries, major US television networks’ news stories and children’s books, including one titled The Lobster Lady, her obituary recounted.

Let’s be clear: I left him over $8 BILLION in reserves. This is the same Mamdani who spent years attacking me for not spending enough during the migrant crisis. The only reason those reserves exist is because I ignored him and his socialist comrades who demanded we blow billions more with no guardrails. “Free” isn’t free. It’s just a bill someone else has to pay.

In the aftermath of Minnesota’s Signal networks being exposed, a ripple effect has surged through activist circles, prompting rapid organization in states hungry to fortify their “defenses” against ICE. Seattle’s groups, for instance, have ramped up encrypted recruitment, drawing from MN’s exposed tactics to create tighter vetting processes and decentralized “response pods” that activate within minutes of raids. Illinois follows suit, with chats buzzing about mirrored databases for agent tracking, now layered with anonymity tools to evade scrutiny. Even in corners like Texas and California, pop-up networks echo the model, blending local intel with national coordination to disrupt deportations.

was an eyewitness as the Financial Times went woke and I couldn’t bear it. The London Stock Exchange Group has cancelled its Financial Times subscription and I can’t blame it

Delusional optimism is a secret to success. People who overestimate their chances work harder and persist longer. Even against the odds, that extra persistence turns failures into wins.

Chinese officials and automakers are eyeing German factories slated for closure and are particularly interested in Volkswagen’s sites (VOWG_p.DE), opens new tab, a person with knowledge of Chinese government thinking told Reuters. Buying a factory would allow China to build influence in Germany’s prized auto industry, home to some of the oldest and most prestigious car brands, the person said.

American bus stops are often significantly closer together than European ones. The mean stop spacing in the United States is around 313m, which is about five stops per mile. However, in older, larger American cities, stops are placed even closer. In Chicago, Philadelphia, and San Francisco, the mean spacing drops down to 223m, 214m, and 248m respectively, meaning as many as eight stops per mile. By contrast, in Europe it’s more common to see spacings of 300m to 450m, roughly four stops per mile. An additional 500 feet takes between 1.5 and 2.5 minutes to walk at the average pace of 2.5 to 4 miles per hour.

“The national interests of countries like the US and Russia won’t always match up. Most of the time, they won’t. But when they do overlap, it would be a mistake, a serious mistake, not to use that moment to agree on practical and mutually beneficial projects: in the economy, trade, investment, and so on.”And then he added: when US and Russian interests don’t align, it would be criminal to let that disagreement slide into confrontation. Especially a direct, “hot” confrontation.

The bottom line is two-fold: 1) the tag team failed to overthrow the regime in Iran, although it surely has not given up on that goal; and 2) there is good reason to think that Israel and the US did not win the12-Day war.

@SenFeinstein abused her Desert Protection Act to close down America’s most profitable Mountain Pass mine in the Mojave in 2002. Her husband Blum was exclusive importer of rare earth metals from China

Verizon has started enforcing a 365-day lock period on phones purchased through its TracFone division, one week after the Federal Communications Commission waived a requirement that Verizon unlock handsets 60 days after they are activated on its network.

In June 2007, Marc Andreessen published what became the defining essay on startup strategy. “The Only Thing That Matters” argued that of the three elements of a startup—team, product, and market—market matters most. A great market pulls the product out of the startup. The product doesn’t need to be great; it just has to basically work.

Mark Carney cannot simply return to Parliament and expect, as he has for the past year, that re-announcing projects or creating new bureaucracies will suffice to fix Canada’s woefully inadequate military, underdeveloped natural resources, and entrenched internal trade barriers. Small ball and tinkering is not going to cut it.

The state told Marin it needed to plan for 14,000+ new homes (a ~12% increase in a county with ~115K homes). The county nodded. Then it upzoned a few dead malls and commercial sites, leaving 99% of its residential land untouched

In 2018, for instance, the West Michigan Woman Brilliance Awards named her woman of the year. In 2020, Gov. Gretchen Whitmer appointed Ezeh to the executive committee of Michigan’s Early Childhood Investment Corporation. In 2021, Aquinas College honored the Nigerian fraudster with its Distinguished Service Award. The acclaim and upward mobility evidently weren’t enough for Ezeh, who decided to live a jet-set lifestyle at taxpayers’ expense. According to a 2023 whistleblower complaint, Ezeh used various interrelated organizations to funnel hundreds of thousands of taxpayer dollars to herself as well as to friends and family members while serving as CEO of the Early Learning Neighborhood Collaborative.

“I think Ken Howery was an effective ambassador to Sweden several years back. I absolutely believe in the private-sector experience,” said Rufus Gifford, who served as President Barack Obama’s ambassador to Denmark and was a top fund-raising official on Vice President Kamala Harris’s presidential campaign.

RGGI forces its member states to buy emissions credits…from RGGI. It’s a non-profit-run carbon tax system. Those credits then get charged directly to you on your electric bill. Youngkin pulled Virginia out of RGGI and saved Virginian’s nearly a billion dollars on their electric bills.

Before you go writing off Virginia know this, Abigail Spanberger has been groomed to run for President(the new Hillary). Being governor is just a stepping stone. So while everyone is distracted with Gavin she is the plan. The VA Legislature will push crazy, radical stuff&she will veto some of it to appear moderate.

Unlike other megaconstellations, including SpaceX’s Starlink, Blue Origin’s new constellation will not serve consumers or try to provide direct-to-cell communications. Rather, TeraWave will seek to serve “tens of thousands” of enterprise, data center, and government users who require reliable connectivity for critical operations.

The U.S. Department of Homeland Security is highlighting the worst of worst criminal aliens arrested by the U.S. Immigration and Customs Enforcement (ICE).

Europe is pathetic at getting anything done. Strategically weak Prevaricating. Disunited. Naive. A confused gaggle of middle managers waiting for distinct leadership, all looking to one another for answers because nobody seems to have any. Clinging onto rules and treaties that are no longer fit for purpose rather than actually using instinct and confidence, as it is the only foothold the lemming-like bureaucrats have to help formulate decisions.

ICE did NOT target a child. The child was ABANDONED.

Tons of headlines from Davos. Here’s a quick run down…

A 2024 filing shows the group awarded just $158,811 in grants that year while Armstrong brought in a salary of $215,726

Bugs Apple Loves: Why else would they keep them around for so long?

Downtown Denver’s office vacancy rate grows to 38.2% as tenants reimagine the workplace

SFPark: interactive map of SF parking regulations.

Got on the Red line in Chicago. One car had guy living in his own shit, sprawled out in his filth eating Chinese take out food, and the car smelled like it. The other had two guys openly smoking joints yelling about the Bears. I chose the shit car because I didn’t want to get into an argument about Caleb’s lucky toss since that might have ended with one of us being stabbed. Thanks Chicago for such luxurious choices.

Due to massive demand, I’ve added English subtitles to the German Amelia/Maria video. Now the message can be understood worldwide

Police at my stop tell me they can’t/won’t do anything. Why give him a ticket when the judge will toss out it anyways.

The lawsuit alleges the companies accessed patient medical records and then sold them to lawyers who sifted through the files to identify potential clients. These companies are “exploiting health information exchange frameworks to fraudulently access and steal sensitive patient health information for financial gain,” the lawsuit argues.

Veterans generally understand the prevalence, presence and immediacy of danger intuitively. This is a trait they share with LE. For example, as a veteran I plan to never again enter the Minneapolis/St. Paul region, ever.

And here’s the hard truth we’ve lived, the people shouting loudest about “protecting immigrants” and hating on ICE don’t actually care about immigrants like us. They care about looking morally superior. That’s it.

Did you know that we fought an entire war in Somalia with 28,000 troops? No. How could you? For you are on the “inside” and unable to see the whole of the host. The host does not want to see itself. If it could, then it would see itself for the bloated, obese, grotesque monster that it is, a monster that has ravaged nearly every small country in the world.

Apple’s annual spend at TSMC grew from $2B in 2014 to $24B in 2025. That is 12x in 12 years. Apple went from 9% of TSMC revenue to 25% at its peak and settled to 20% in 2025. More striking is Apple’s dominance at node launches: consistently >50% since 20nm and in some cases near 100%. Apple effectively funded the yield learning curve for every major node transition since 20nm.

But there’s a small workaround that seems to work. Browsers won’t delay the loading of an image if it’s already been fetched. You can take advantage of that by conditionally preloading the image using a media query, then marking the image as lazy later. I tested it using the HTTP link header, but may also work fine with a <link rel="preload"> tag.

The Remnant: The Last Christians of Denmark is an independent documentary film exploring the lives, hopes, and challenges of traditional Christian families in one of the world’s most secular nations.

Too often, technology becomes obsolete before the procurement cycle even finishes. The thesis of Klein and Thompson does not simply apply to FAA acquisition; it explains why so many modernization efforts languish or fail.

What I am saying is that I, nor anybody, can tell the difference between the conference coverage and a very well-executed hoax. Consider that the Great Moon Hoax was walking a very fine tightrope between giving the appearance of seriousness, while also not giving away too many details that’d let the cat out of the bag. Here, the conference rhymes.

“We don’t want to be perpetual renters of disposable crap,” she told an interviewer for the website Front Porch Republic. “We want things that last.”

Like Houellebecq and Céline, however, Obertone’s literary reputation is difficult to separate from his political positions. Houellebecq once described Islam, the faith of many French people of immigrant origin, as “the dumbest religion.” He later published a novel imagining France under the rule of a Muslim president whose title—Submission—mischievously alluded to the Arabic etymology of “Islam.” Obertone, for his part, has been highly critical of immigration’s impact on French society and has ties to “great replacement” theory. His three-volume novel, Guérilla (published between 2016 and 2022)is the story of France’s descent into civil war following an uprising of racial minorities.

The booming second-hand luxury market and stricter anti-money-laundering regulations have intensified this scrutiny. As one sales associate at a major Paris boutique told Glitz, “Every new client is automatically a suspect.” Staff now collect and assess far more data than before, from home addresses and their perceived prestige to social media activity and online presence. Sales associates are trained to evaluate whether a client’s buying journey appears coherent.

There were 372 distinct emojis used within 4162 notes (Figure). Approximately one-quarter (1011 notes [24.3%]) contained more than 1 emoji (maximum?=?32; median?=?4). Emoji usage rates remained mostly stable at 1.4 notes with emojis per 100?000 notes from 2020 to 2024, increasing to 10.7 per 100?000 notes by quarter 3 of 2025.

Another big court win against the very corrupt Wisconsin State Attorney General Josh Kaul and his lackey Dane County District Attorney Ismael Ozanne. Surprise ending.